With last year’s addition of Nubank, the number of Latin American companies in the F-Prime Fintech Index grew to five, including PagSeguro, MercadoLibre, Stone, and dLocal. The F-Prime Fintech index is designed to track the performance of emerging, publicly traded financial technology companies.

While the public market correction over the last twelve months has been broad, tech and fintech stocks have seen the largest declines — the Fintech Index was down 72 percent in 2022. The decline is especially pronounced for the 10 largest exits during the peak years of 2020 and 2021, including dLocal (down 77 percent) and Nubank (down 54 percent).

Despite the correction, scaled LatAm fintech companies (those with more than $5B in market cap) are still growing at high rates. Nubank grew LTM revenue by 117 percent while MercadoLibre grew 54 percent, outperforming the 48 percent average across the Fintech Index.

Payments Lead the Way

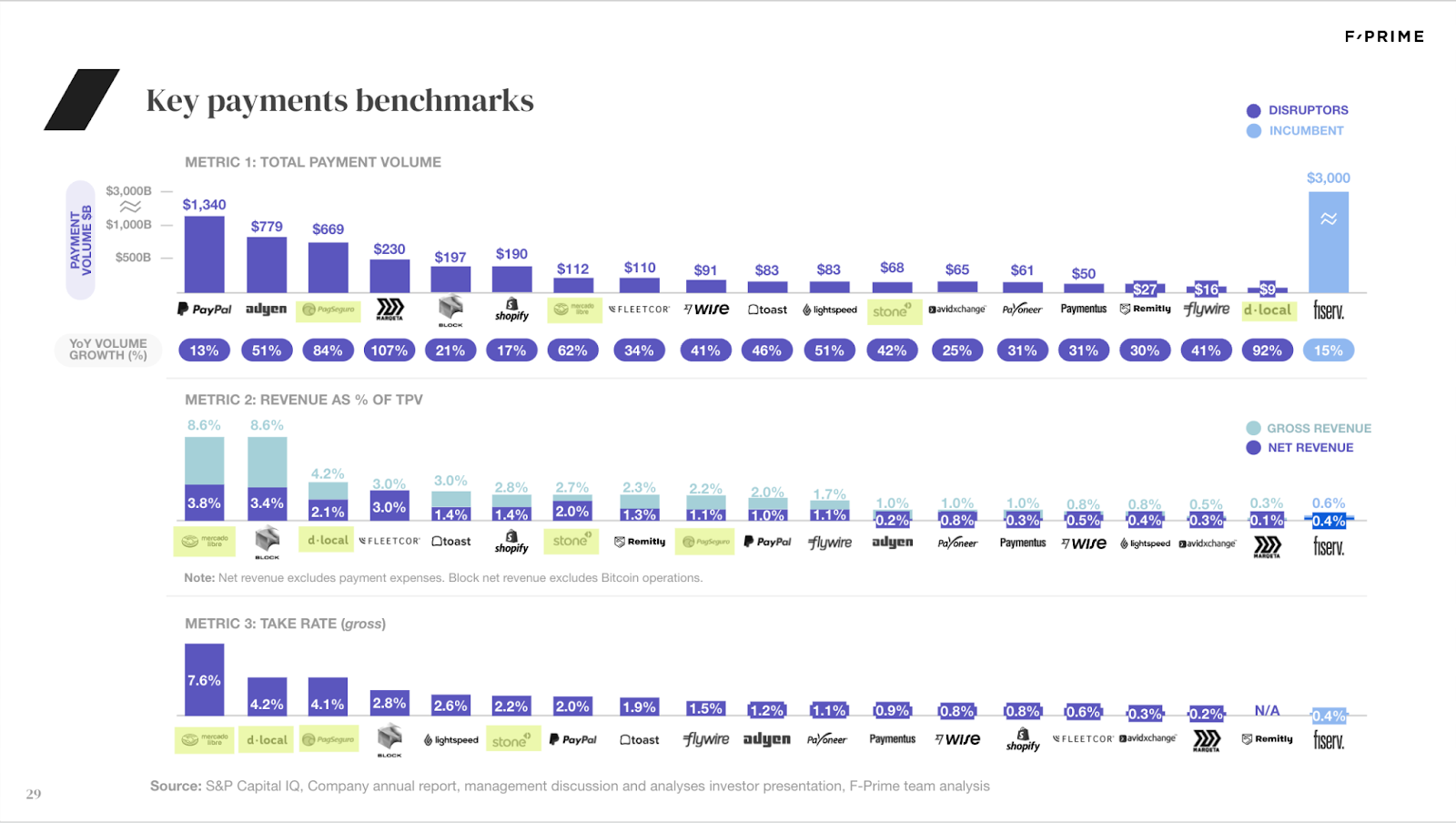

Four out of five Latin American companies in the Fintech Index (PagSeguro, MercadoLibre, Stone, and dLocal) have a payment business model. In fact, PagSeguro’s $669B in annual payment volume — 84 percent more than 2021 — was third-largest in the sector last year.

Thanks to its diverse revenue streams — which range from payment processing commissions and mobile point-of-sale products to consumer loans — MercadoLibre had the highest gross revenue as a percentage of total payments volume, at 8.6 percent. Second-highest was dLocal at 4.2 percent, followed by Stone at 2.7 percent, and PagSeguro at 2.2 percent.

LatAm payment service providers also command the highest take rates, ranging from PagSeguro’s 4.1 percent to MercadoLibre’s 7.6 percent — far higher than the one-to-two percent take rates in the United States. There are a couple of factors that might explain the higher take rates in Latin America, including the higher cost of service delivery in the region and a lack of alternatives. However, the cost to deliver services is likely much higher in LatAm, dampening those net take rates.

Banking Thrives with the Super App Model

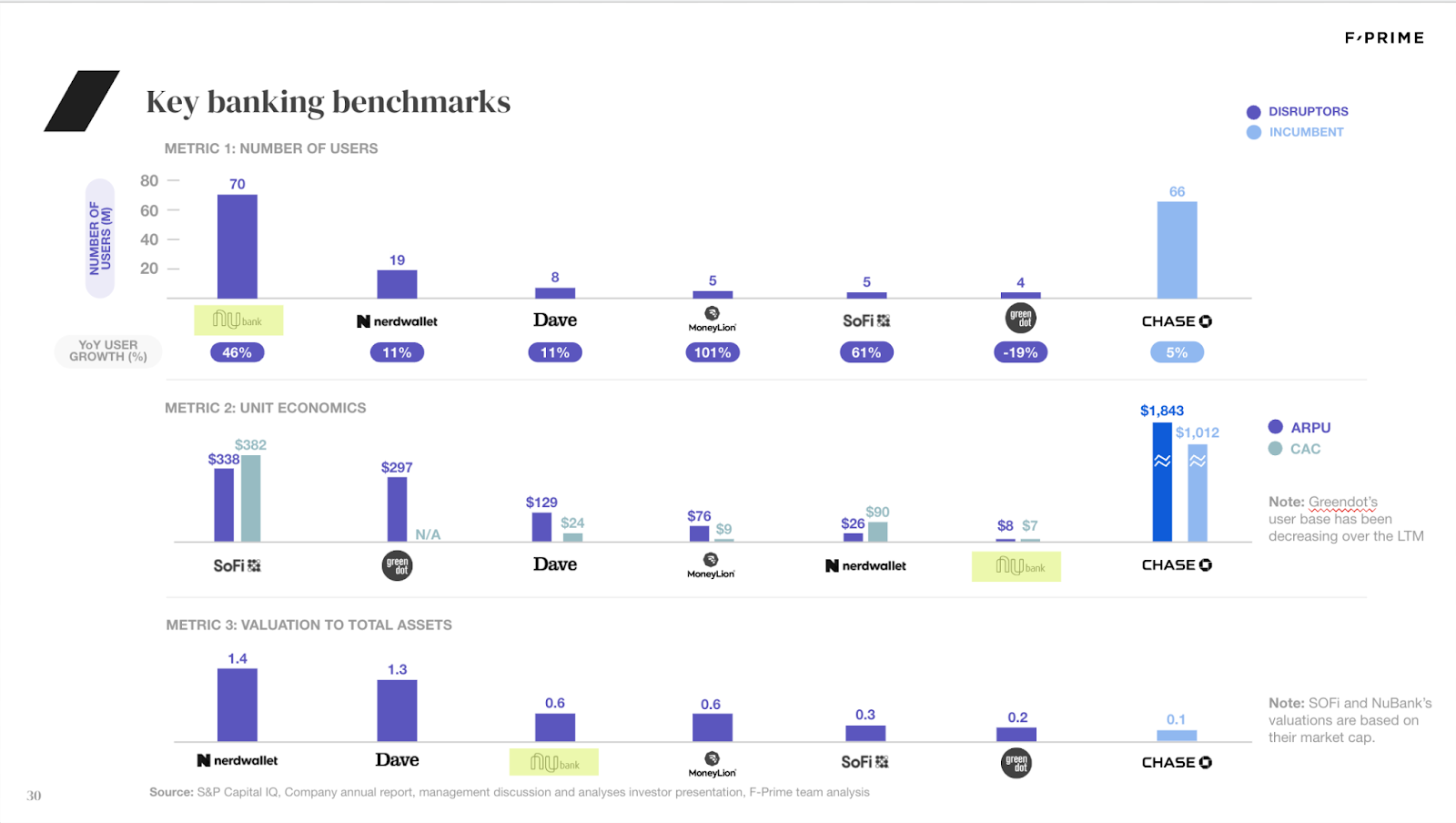

Nubank has more users than any other neobank globally with an incredible 70 million users — more than Chase, an incumbent bank with 66 million users. Given the low banking penetration in the region and the underserved nature of the local population, the ceiling is really high for Nubank.

The company has become a financial super app, an achievement that US counterparts like Chime or Dave must envy. The financial super app model (being a one-stop shop for all customers needs) tends to resonate better in emerging markets. Nubank enjoys an average of 3.8 products adopted per active customer thanks to its “compound of cross-sell” — pitching bank accounts, credit cards, investment accounts, and loans to existing customers.

Bright Outlook

Although LAVCA reported a 50 percent drop in VC investment compared to 2021 — from $7.8B in 2022 to $15.9B in 2021 — fintech remained the leading sector for capital invested. The category captured 43 percent of all dollars in 2022, up from 39 percent in 2021.

Meanwhile, Latin America still reached all-time seed stage records across all major markets despite the overall pullback. Seed funding has always proved resilient through downturns, and this time around a growing number of local fund managers continued to invest in early entrepreneurs.

While it takes time for LatAm companies to mature and exit in public markets, we remain active and optimistic about the region’s startup ecosystem at the earliest stage.